Our Approch

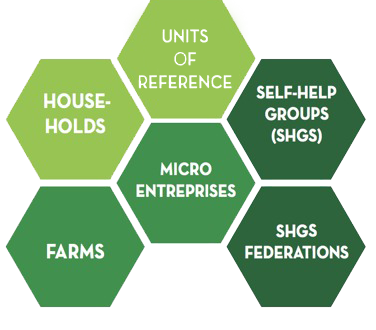

DART™ applies ratings across a range of criteria to assess household and community institutions.

More than 13 million micro are led by women in India (500 million Micro Small Enterprises Globally

Lack of data about borrowers impairs their ability to access affordable, timely and cost-effective credit, leading to financial exclusion

Financial institutions are unable to reach the unbanked & underserved and provide service on a cost-effective and sustainable basis due to:

- Lack of relevant data about nano, micro, and small borrowers

- Errors in data when collected, stored and transmitted to decision makers

Around 220 million rural Indians remain unbanked consisting of small and marginal farmers, Nano, micro, and small entrepreneurs especially women

- 50 % women in India use their bank account in a limited manner or not at all

- 24% lack access to formal financial services.

Ministry of Micro, Small & Medium Enterprises (MSME) present an unmet demand of almost Rs. 25 trillion in India

- less than 5 % of MSMEs have access to formal credit

- As per Macro Finance Institutions Network (MFIN) estimates: Microfinance reaches < 20 % of potential households in India

Marginal Farmers, Nano, Micro and Small entrepreneurs especially women play an important role in raising agricultural development and achieving inclusive growth

We provide an authentic scoring mechanism based on extensive analytics of data, collected at the family and group level which is both quantitative and qualitative.

We offer data analysis, rating and tracking services to banks, micro-finance institutions, P2P platforms and governments interested in lending to the financially excluded. We do Individual and Institutional ratings.

Insights derived from the analytics help us to achieve a granular understanding of households and last mile institutions, thus allowing us to take a more deliberate approach and design customized services. We offer the following:

DART™ can be used by third parties to maintain a comprehensive database of financial and non-financial data for their beneficiaries.

DART™ applies ratings across a range of criteria to assess household and community institutions.

Through our partners, we reach out to last mile institutions, underserved households and women enterprises by providing them financial literacy, business planning skills, risk reduction strategies, and capacity of the SHGs & federations to serve their member households

Is on women’s social, financial and economic empowerment, and we are primarily working with women-led livelihood groups and federations in India. Women are at a greater risk of increasing indebtedness as a majority of micro-finance borrowers are women. We work towards building their resilience to financial shocks by increasing their awareness of their own financial status, building their credit history, managing their savings, and helping them track their performance.

Their ability to develop and scale entrepreneurship activities are constrained due to poor access to financing options, lack of knowledge, and no or limited access to technology.

At the household level, DART™ focuses on:

At an institutional level, DART™ focuses on increasing capacity of women to:’

lies in partnering & collaborating with agencies that bring sustainable changes to underserved households & communities.

We do this by helping our partners strengthen the last mile institutions and build grassroots leadership, which will be there for generations to come. We believe it will ultimately bring down cost of financial services to the poor.

The strength of a household lies in the strength of the communities to which they belong.

By working through trusted partners, we are able to adapt to the real needs of customers and families, whether that’s helping farmers adapt to climate change or finding ways to engage with women and youth.

Adding {{itemName}} to cart

Added {{itemName}} to cart